Understanding Startup Equity, Dilution, and Valuation

A Guide to Navigating Equity, Dilution, and Valuation Dynamics

What is Equity?

Think of startup equity like a piece of a pie. The whole pie represents the entire company, made up of shares or ownership percentages. At the beginning, founders have the whole pie. The way they divide it, especially if there are co-founders, can be 50/50, 60/40, 30/30/30, 70/30, based on things like time, money, and expertise.

Startup equity shows who owns what part of the company, and it's shared among founders, investors, advisors, and employees.

Things get interesting when startups need money to grow and hire more people. Investors want a piece of the pie in exchange for the money they put in. In the early stages, they might ask for more because they're taking a bigger risk on an idea that hasn't fully taken off. As the startup gets more funding in later rounds, the amount of the pie given to investors goes down. But every time more money comes in, the founders' share of the pie also goes down. It's like diluting the ownership a bit, but it's a trade-off for getting the funds needed to make the company grow.

What is Dilution?

So, when founders talk about the company diluting in funding rounds, it basically means that their ownership stake in the company decreases. Here's the lowdown on how it happens:

Imagine we're at a point where the company needs more money to grow, maybe hitting a new milestone or expanding into new markets. That's when the company decides to raise capital through a funding round – you might have heard of these as seed rounds, Series A, Series B, and so on, each stage representing a different phase of the companies growth.

Now, in order to bring in that extra cash, the company has to issue new shares of the company to investors participating in the funding round. These new shares are like a piece of the ownership pie.

Here's where the dilution comes into play. When those new shares are issued, the total number of shares in the company goes up. If founders or people with existing equity don't buy enough of these new shares to keep their ownership percentage the same, the slice of their pie gets smaller – that's the dilution part.

But, here's the deal – dilution is a necessary part of the game. It's how a company gets the funds needed for things like hiring top talent, investing in product development, or expanding its reach. Investors put money into the company, and in return, they get a piece of ownership.

The key for founders is to strike the right balance. Carefully consider the terms of the funding round, the valuation of the company, and how much of ownership they’re comfortable giving up in exchange for the capital or expertise injection.

What is Valuation?

Valuation of a company is a process of determining the total value (worth) of the company.

Imagine the company starts today with X number of initial shares, the valuation of that company is likely to be zero as the company neither has assets, nor the revenue.

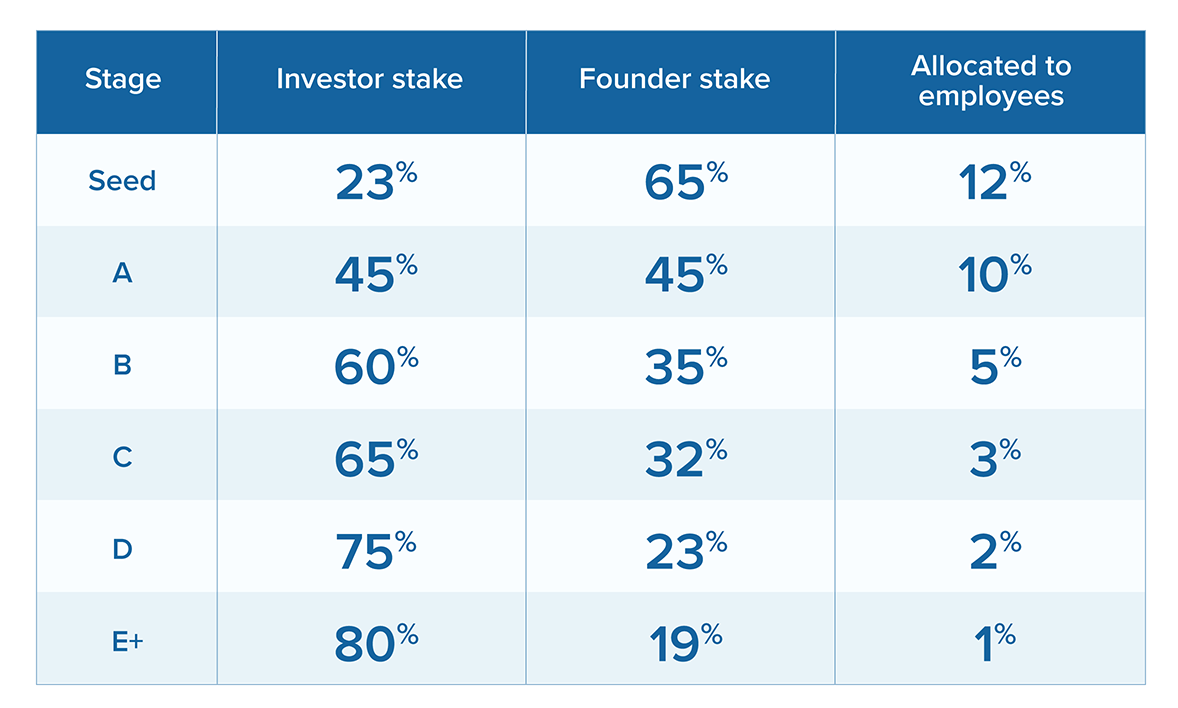

Btw, usually the initial equity distribution is decided at or shortly after that point, so how do we determine who gets how much of equity?

The following chart by Gust, is based on 2016 data that gives a good idea of how equity is distributed among different stakeholders.

Aside from that, there are some indicators based on which the valuation of the company is determined at the early stage.

Look at the valuation of the existing similar companies in the market and have some assumptions on some variables.

Look at the existing assets, estimate future revenue & profit projections, using methods such as Comparable Company Analysis (CCA) and Discounted Cash Flow (DCF), etc.

As the company grows, the there are more indicators of determining its valuation. Here’s a breakdown of how the valuation is usually determined at different stages of a startup.

1. Pre-Seed Stage

Methodology: Valuation at the pre-seed stage is highly subjective and may involve a qualitative assessment.

Example: A startup with a unique AI algorithm might be valued based on the founder's expertise, the algorithm's potential applications, and early interest from industry experts. Comparable deals could include early-stage investments in similar deep tech ventures.

2. Seed Stage

Methodology: Valuation still involves qualitative aspects but starts to incorporate quantitative factors like user metrics.

Example: A seed-stage SaaS startup with a functional prototype and initial user adoption may be valued at $2 million. This valuation could be influenced by the startup's Monthly Recurring Revenue (MRR), customer acquisition cost (CAC), and a comparison to similar SaaS companies at a similar stage.

3. Series A

Methodology: More quantitative metrics come into play, including revenue multiples and detailed financial analysis.

Example: A Series A e-commerce platform with $5 million in ARR (Annual Recurring Revenue) might be valued at around 5x ARR, resulting in a $25 million valuation. Investors may also consider factors like customer retention rates, customer lifetime value (CLV), and the total addressable market (TAM).

4. Series B and Beyond

Methodology: Emphasis on financial metrics intensifies, and valuation becomes more data-driven.

Example: A Series B biotech company with significant revenue growth and a unique drug in the pipeline could be valued at $150 million. This valuation might be based on a combination of revenue multiples, EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization), and the company's position in the market compared to competitors.

Factors Influencing Valuation

Market Potential: A fintech startup targeting a rapidly growing market with a $10 billion total addressable market (TAM) might command a higher valuation.

Revenue and Traction: A Series A software company with a 50% month-over-month growth rate and $10 million in ARR could justify a higher valuation.

Team: A team with a successful track record in scaling startups may positively impact valuation.

Negotiation and Terms:

Example: Founders might negotiate a higher valuation by offering investor-friendly terms like a lower liquidation preference or more favorable anti-dilution protection.

External Factors:

Example: Economic downturns may result in lower valuations across the board, impacting the negotiating power of both founders and investors.

Thanks for reading my post! Let’s stay in touch 👋🏼

🐦 Follow me on Twitter for real-time updates, tech discussions, and more.

🗞️ Subscribe to this newsletter for weekly posts.